What is a rolling forecast? Templates, Guidelines and Benefits

Revenue and expenditure are set out for the next 18 months and are updated every quarter, firming up the short-term numbers for the next three months and updating the annual forecast. Whilst initially this was performed monthly, over the last ten years it has evolved to a quarterly process. Only operations with wildly fluctuating revenues and expenses need to retain a monthly update, e.g. subject to commodity prices, exchange rates that can change a month-end result by over 20% etc. It is the first step to replacing the antiquated and static annual planning process.

What is quarterly rolling forecasting (QRF)?

Quarterly rolling forecasting is a process where management sets out the required revenue and expenditure for the next 18 months. Each quarter, before approving these estimates, management sees the bigger picture six quarters out. All subsequent forecasts, while firming up the short-term numbers for the next three months, also update the annual forecast. Budget holders are encouraged to spend half the time on getting the details of the next three months right, as these will become targets, on agreement, and the rest of the time on the next five quarters.

The quarterly forecast is thus used to:

- Fund budget holders, on a quarterly rolling basis, once their forecast has been approved

- Set the monthly budgets to be used for month-end reporting (set only one quarter ahead)

- Update the annual forecast

- Give a view of the next financial year

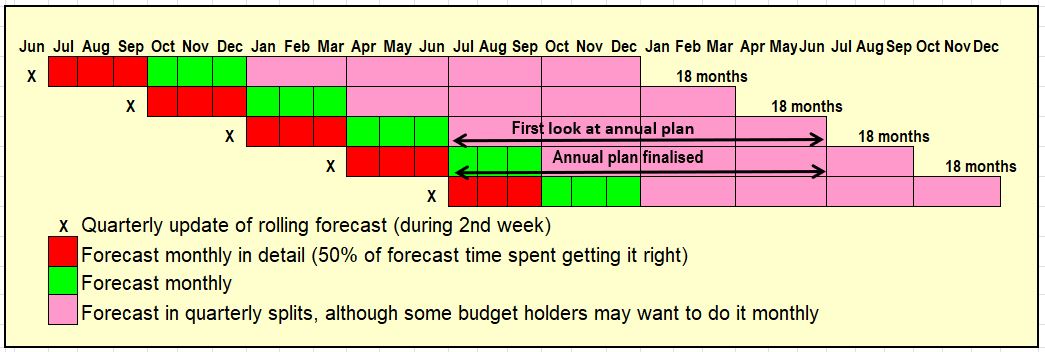

Each quarter forecast is never a cold start, as budget holders have reviewed the forthcoming quarter a number of times. With the appropriate forecasting software, management can do their forecasts very quickly; one airline even does this in three days. The recommended elapsed time spent on the four quarterly forecasts during any given year is no more than five weeks. Exhibit 16.2, from my book, shows how the quarterly rolling process works for a June year-end organization.

Exh 16.2 How the rolling forecast works for an organisation June year-end

Exh 16.2 How the rolling forecast works for an organisation June year-end

The dark shaded zone is the forecast for the next quarter and the most important part to get right. The light shaded zone is the second quarter. Quarters one and two will be forecast monthly and quarters three to six are forecast in quarterly blocks as less detail is required. As a guide, budget holders should spend 60 percent of their time on the

first quarter because first quarter numbers will become targets, 20 percent on the second quarter and 20 percent on the remaining four quarters. Most organizations can use the cycle set out in Exhibit 16.2 if their year-end falls on a calendar quarter end. Some organizations may wish to stagger the cycle say May, August, November, and February. An explanation of how each forecast works, using a June year-end organization, follows.

The Process Quarter by Quarter for June Year-End Organization

December update (takes one-week) In the second week of December, budget holders forecast to the end of the year, with monthly numbers, and the remaining period in quarterly breaks. Budget holders obtain approval to

spend January-to-March numbers subject to their forecast, still going through the annual plan goalposts. The budget holders, at the same time, forecast next year’s numbers for the first time. Budget holders are aware of the expected

numbers, and the first cut is reasonably close. This is a precursor to the annual plan. This forecast is stored in the forecasting and reporting tool. This update process should take only one elapsed week.

March update and annual plan (takes two weeks) In the second week of March, budget holders re-forecast to year-end in monthly numbers and we should be able to eliminate the frantic activity that is normally associated with

the spend-it-or-lose-it mentality. They also forecast the first quarter of next year with monthly numbers, and the remaining periods in quarterly breaks. The budget holders at the same time revisit the December forecast (the previous forecast) of next year’s numbers and fine-tune them for the annual plan. Budget holders know that they will not be getting an annual lump-sum funding for their annual plan. The number they supply for the annual plan is guidance only.

For the annual plan, budget holders will be forecasting their expense codes using an annual number and in quarterly lots for the significant accounts, such as personnel costs. Management reviews the annual plan for next year and

ensures all numbers are broken down into quarterly lots. This is stored in a new field in the forecasting and reporting tool called “March ___ forecast” This is the second look at the next year, so the managers have a better understanding.

On an ongoing basis, they would need only a two-week period to complete this process.

June update (takes one week) Budget holders also are now required to forecast the first six months of next year monthly and then on to December in the following year in quarterly numbers. Budget holders obtain approval

to spend July-to-September numbers, provided their forecast once again passes through the annual goalposts. This is stored in a new field in the forecasting and reporting tool called “June ___ forecast.” This updated process should take

only one elapsed week.

September update (takes one week) Budget holders reforecast the next six months in monthly numbers, and quarterly to March 18 months forward. Budget holders obtain approval to spend October-to-December numbers. This is stored in a new field in the forecasting and reporting tool called “September ___ forecast.” This updated process should take only one elapsed week. You will find that the four cycles take about five weeks, once management is fully conversant with the new forecasting system and processes.

Also read

- 7 Rolling forecasting templates

- 12 rolling forecast lessons

- 9 reasons why you should migrate from forecasting spreadsheets

- The 10 benefits of quarterly rolling forecasting process

- 7 tips to speed up forecasting

- 14 Foundation stones of a Quarterly Rolling Forecasting

For more details access my toolkit How to Implement Quarterly Rolling Forecasting and Quarterly Rolling Planning – and get it right first time // Toolkit (Whitepaper + e-templates)

You can have a look inside the toolkit